In the aftermath of the 2007-2008 financial crisis, two Congressmen came up with a law to make U.S. banks safer in order to protect Americans.

Chris Dodd, a Democratic Senator for Connecticut, and Barney Frank, a Democratic representative for Massachusetts, worked together to create the Dodd-Frank Act: a bill that put stricter requirements on the banks.

Frank called it the “toughest financial reform and regulation since the New Deal.” “We were fighting an ongoing set of practices, and if we didn’t put an end to them, they would have kept going,” he said.

Dodd added, “What we tried to do with the bill is not eliminate future crises — they are going to happen — but create tools. New tools, the ones that [Fed Chair Ben Bernanke] and [Treasury Secretary Henry Paulson] claimed they didn’t have.”

Frank, who has retired, currently sits on the board for Signature Bank, while Dodd recently joined the law firm Arnold & Porter.

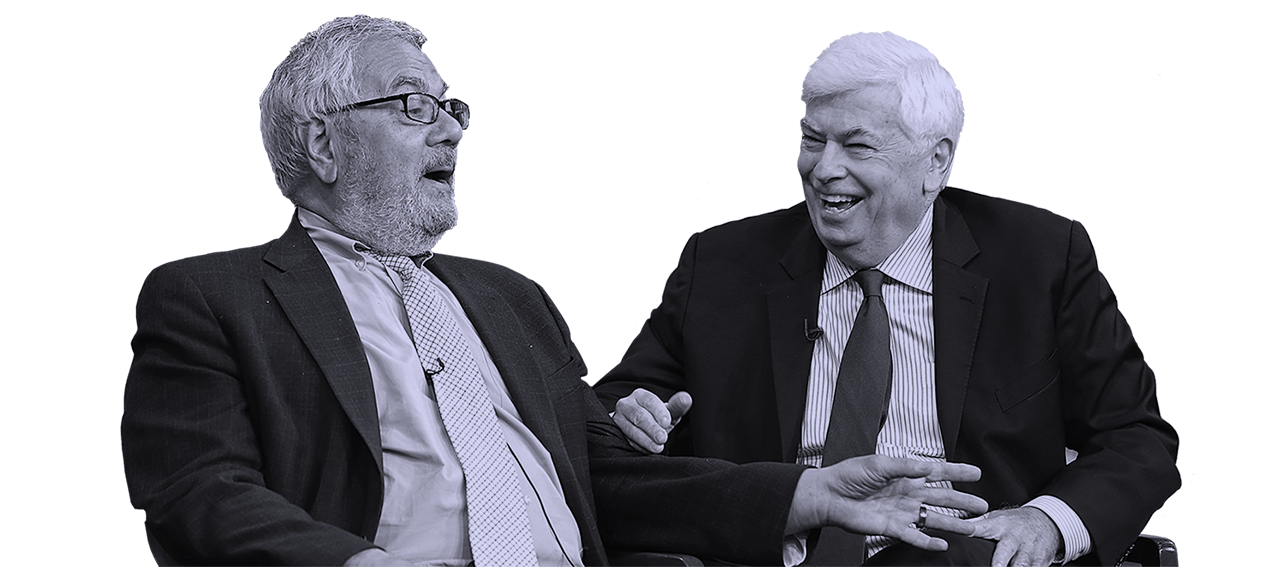

Marketplace host David Brancaccio interviewed both of them on Sept. 12 in Washington, D.C. about whether Americans would support another bailout, the future of the Dodd-Frank Act, and whether the financial crisis led to the rise of Donald Trump.

The following video and edited transcript of their conversation is part of our Divided Decade project covering the 10-year anniversary of the financial crisis.

David Brancaccio: Sen. Chris Dodd, Congressman Barney Frank, thanks for joining us.

Barney Frank: You’re welcome.

Brancaccio: All right, let's just get into the mindset of back then ten years ago. Each of you, I think has long and repeated experience dealing with emergencies, but when and where did it become clear to you that you were fighting the worst financial crisis in generations?

Chris Dodd: Well, I think it was beginning of ‘06. We talk about the crisis of ‘08, but really contrary to what people think, this was not a secret, the housing bubble. As early as ‘06, in fact Jack Reed, Sen. Reed of Rhode Island and Jim Bunning, of all people. Bunning chaired the subcommittee dealing with housing. They had hearings in ‘06 on the growing problem of the housing bubble, but it wasn't really until ‘07, into ‘07. And then it was Bear Stearns which really kind of blew things up, but there was a lot of — we had 90 hearings in the Senate in ‘07 on the housing crisis coming about. Ninety hearings is a lot of hearings. So we're very much aware of the problems growing.

Brancaccio: Didn’t you have years and years, Congressman, in dealing with housing issues? You were tracking this too, right?

Frank: Yeah, and Chris is right. We were onto the housing thing. In fact, in my first year as the chairman of the committee, 2007, when the Democrats took over, we actually passed a bill that would have shut down the bad housing and it was Republican opposition, meant you couldn't break a filibuster in the Senate. But actually there's this conservative myth that the problem was that liberals were pushing to put poor people into housing and that’s what caused the problem. The exact opposite is the case. Beginning in ‘94, Congress passed a bill the last time the Democrats had control, until back to 2007, which mandated the Federal Reserve to restrict that. Alan Greenspan refused to do it. Greenspan said, “No, I believe in the market.”

Brancaccio: This is in the 1990s, right? He got the power to do it —

Frank: In 1994. And then in the late ‘90s, a number of states began to do this because the federal government wasn't. And the Bush administration used the federal power of preemption and cancelled the ability of the states to do it. So then, when the Democrats get control, there are hearings, as Chris mentioned, that he's holding. We actually passed a bill. The Republicans were still against it. The Wall Street Journal — and I love this — in November of 2007, the Wall Street Journal attacked me by name because we were trying to restrict subprime loans. And they said, why doesn't he want poor people and minorities to take over? So I will say this, I think we saw the housing issue. We didn't see how much it was going to spread. But then Chris is exactly right, when Bear Stearns had to be taken over, that was a sign that this had spread beyond housing.

Brancaccio: And then in the fall you get Lehman. But is there a meeting where Treasury comes over and says, “No, no this is happening now, it's starting to fall apart?”

Frank: Well, during the summer, I would get phone calls on Friday afternoon from Paulson, generally after the markets had closed, sort of, “oh, we got this problem.” Remember there was a problem where Citicorp was a problem, and then there was a problem where Wachovia was a problem, and they had Wachovia be taken over by Wells Fargo. Then there was the Merrill Lynch, that was taken over by Bank of America. There was a series of potential failures and they found some way to resolve it, starting with Bear Stearns. But then came Lehman, and there was nobody left to resolve it with. But we saw this building up.

Dodd: Well, we did, but the administration was slow. I mean the idea that it was one ant in the kitchen. I mean that this is somehow, that this was a one-off problem and that it wasn't a systemic problem.

Brancaccio: This is the late George W. Bush administration at that moment.

Dodd: Yeah. He was very unpopular and leaving office, and so that made it difficult. But that was — Hank Paulson, look, he had come out of Goldman Sachs, very knowledgeable, smart, not a Washington person. And so it was uncomfortable, I think, in many ways with the politics of the town, in a sense, and wanted to keep the ball in the air, be positive, and this was all going to work out, and positive statements. When in fact, it was going the opposite.

Frank: I had a somewhat different reaction to Paulson. And you are right to mention Bush. I mean the problem is, I think Paulson did begin, and Bernanke, to see this. Although, Bernanke had earlier said, he acknowledged, “oh this is housing, it's not going to spill over.” But I think they began to see that this could be more of a problem. They were telling me they were worried they didn't have the tools, but you had this very conservative administration. And, by the way, when Bernanke and Paulson did intervene to keep Bear Stearns from failing, and had JPMorgan Chase take it over, the Republicans on the committee that I chaired — very, very conservative — wanted me to have hearings so they could denounce Paulson and Bernanke for their intervention. I wouldn't have the hearings, I didn’t think it was going to be kind of useful.

Brancaccio: Who, by the way, is working fairly fluidly with his present, with their president who is a Republican, nonetheless.

Frank: But this was a tension that Paulson faced, which was, you know, the Republican Party was so resistant. And I do think they had a series of fixes, we’ll will fix this, we’ll fix that. Paulson and Bernanke were saying to me at least, well we would like to have a better set of tools. And I think in the end though, you know, they had JPMorgan Chase take over one, and Bank of America took over another, and Wells Fargo took over another, and then came Lehman, and there was nobody left to take it over.

Brancaccio: Did you have the right resume to have to deal with this. Did you have the right qualifications and expertise to do this kind of work?

Dodd: Well, probably no one did, in the sense we were dealing with a set of issues and problems that hadn't surfaced. Obviously the industry had become far more sophisticated, outstripped the capacity of the regulators and rulemaking. I think, you know, Paulson is correct and Bernanke, in the sense that the tool chest was not keeping pace with the kind of issues that we’re confronting all the time. And the issue of financial literacy, I've often said it's not only a general problem with the public at large, but you can make the case for the Congress itself. All of a sudden dealing with issues in the derivatives area, for instance, which might as well have been in Latin or Greek, as well as in English. So there was that gap. But there were talented people. As I mentioned, we had 90 some odd hearings in ‘07, not to mention ‘08, and a lot of very talented people coming up and warning about the problems and they were being ridiculed. I remember one guy came up and said there could be as many as a million foreclosures, and he was accused of exaggerating. And he was, he was exaggerating in the sense of the size, it was more like 5 million.

Brancaccio: It was more like 5 million. Did you feel you were in over your head at any point in all this?

Frank: I felt I was being, I mean I didn’t feel, I was being pushed. Well you mentioned my interest in housing, I got on this committee, was then called the banking committee, because I cared about housing. And when I became chairman, you know, I [thought] I could really do something about affordable housing. And, you know, by necessity you had to deal with this. No, I had to do a lot of learning. You know, these things, derivatives were deliberately somewhat obfuscatory, and yeah I almost felt like the teacher who is teaching a subject that's new and you're a day ahead of the class. I mean the night before you teach the class, you got to go read the lesson, and there's a lot of learning there, and you realize how much you pick up. My husband is a surfer, not somebody who had previously been involved in this, but somebody later told him he was the East Coast surfer most knowledgeable about credit default swaps they’d ever met.

Brancaccio: He did the crash course as well. So look we're certainly going be talking a lot about the legislation, Dodd-Frank. But back in the TARP days in that fall of 2008 after Lehman, you're working hard on a response, but what's your biggest regret from that period?

Frank: For me it’s easy, we did put into the bill — and they just wanted the authority to go and do it. And they were worried, and I understand that, although I disagree with it, they were worried, particularly Paulson, that if the heads of the financial institutions were unhappy with the terms, they wouldn't participate [in TARP]. I told them at the time that was the most unpatriotic description of bankers I ever heard. That if we, for example, were to impinge on their bonuses, they would not do what was necessary to save the country.

Brancaccio: So unpatriotic? National emergency and they don’t want to forego?

Frank: Yeah, and we disregarded that, and wrote into things that they didn’t want. But we did write into it explicitly the authority to use some of the TARP money for foreclosures. And what happened was Paulson decided he needed to use the first $350 billion — well, here's the dilemma we had, Chris Dodd, myself, Nancy Pelosi, Harry Reid. You know, and it’s part of the problem of being a Democrat. We believe in government. We believe government has a major role and we're not ready to see things crash because the people we most care about are going to be hurt. People said, “oh, you just bailed out the bankers.” Jamie Dimon wasn’t going to be hurting. He didn't have to go to the ATM, he had enough money put away. It’s the working people who were going to be hurt. So we had to give them the tools, knowing that we couldn't wield them ourselves. But the alternative would have been worse. And one of the problems we had was we told them do something about foreclosure, and [Paulson] refused to do it. And that was my most serious regret.

Dodd: Well, it was you know, people have forgotten this, but we had the meeting on Sept. 18, which of course was that incredible gathering where Ben Bernanke says, and I'm quoting him almost exactly here, “unless you act,” speaking to the congressional leadership, Barney and I, in the room, “in a matter of days, the entire financial system of this country and a good part of the world will melt down.” Needless to say, the oxygen left the room in Nancy Pelosi’s conference room that night. Within a matter of a couple of days, two or three days, at 1:30 in the morning, received a bill. And it was two and a half pages long, said give me $700 billion, no court, no regulator can intervene. I got the call at 6:30 in the morning from staff saying this is — you can't imagine. Imagine Barney and I trying to pass that thing. So began the negotiations out of the bill, what turned out to be about 100 pages long. But we did a number of things in there. And, Barney is absolutely correct. They were not enthusiastic about it. In fairness to them, they were worried that the banks would not participate. But assistance on foreclosure, the warrants, which made us billions of dollars for the taxpayer ultimately.

Brancaccio: In the end.

Dodd: Yeah, but people don’t remember that at all. Tranches, we didn't vote all at once. It was done in parts, so you could actually judge it. Put a jail resident in the process, a Congressional Committee of Oversight, along the way. And the point that Barney just made, I talked to Steve Rattner last night, had we not done what we did beyond the banks and allowed for some of those monies to be used in other economic areas, Chrysler and GM would have failed.

Brancaccio: That’s an interesting point. So this financier, famous Steve Rattner, his point is that if you got the homeowners mortgage relief, it might have impinged on the auto rescue?

Dodd: Some of that money could be used on other things.

Frank: No, no, he wasn't complaining. We wrote it somewhat more broadly, and the way we wrote it was what allowed them to keep General Motors and Chrysler in business. That came out of the TARP.

Dodd: That's part of that. That was part of the negotiation of putting that package way beyond, “give me $750 billion.”

Brancaccio: Oh, I see, you're saying, look you didn't have $2 trillion, you had $700 billion you're working with.

Dodd: Right.

Brancaccio: And it had to be allocated, you tried on mortgages —

Frank: And Chris mentioned the tranches, so the first tranche — which is a fancy congressional word for half — was $350 billion. And we said “you got to use this,” I mean I had a hearing waving the bill at Paulson. And the problem was, Maxine Waters and I, we had to get this bill through the House. Getting it through the House was harder because Chris had a more responsible set of Republicans to work with.

Dodd: Well, only one-third were up [for reelection].

Frank: That's a good point. So we had to really work hard to get this through, and to get the Democrats to support it. Maxine Waters and I stressed that we had foreclosure relief, and then Paulson gets the $350 billion, and I generally work well with him, and think highly of what he did in general, but I disagreed sharply here. He refused to use any of the first $350 billion for mortgage foreclosure relief, saying I need it all keep the banking system going. Even the auto [bailout] had to come out of a second group, another $75 billion. And that's what led people accurately to say, “look you you just bailed out the bankers.” Now, we didn’t bail out the bankers to help the bankers. We did it, as Chris said, to keep the economy from crashing. But, that was the failure. At that point we lost the opportunity to use some of that money to alleviate foreclosures. And let me just say about foreclosure, not everybody who was being foreclosed upon was a worthy recipient. Some people did lie and did take money out.

Brancaccio: Some over-reached.

Frank: But there were some who were victimized, there were many who were victimized and they should have been helped.

Brancaccio: And you know the vote, you know, I hate to bring up a sore subject, but it doesn't pass the first time. It doesn't do it, it takes the Dow Jones Industrial Average falling 2,700 points over a couple of days to, I guess, focus attention?

Frank: Among the Republicans. Remember the Democrats, and this is — people ask, whatever happened to bipartisanship? Barack Obama got elected and the Republicans never gave him the cooperation we gave to George Bush and his administration. And so the Democrats voted heavily for it in the House, Republicans voted heavily against it. And it was only after the stock market dropped 700 points that some Republicans began to hear from their constituents that they better turn around. So in the second vote, a majority of Republicans still voted against it, but enough had switched because of that pressure.

Brancaccio: I mean it's almost not irrational on the part of those Republicans to be leery of voting for the bailout. I mean they got in trouble in their elections that followed.

Dodd: That's always a safe bet. Richard Shelby and I are good friends. But he’ll tell you, he never votes for a bailout. Whether it was New York City, whether it was Chrysler, whether it's —

Brancaccio: Always say no to bailouts?

Dodd: You're not getting into too much trouble by voting no.

Frank: The general way that we characterize that in a legislative body, when there's something you know should be done but it's unpopular, you vote no and pray yes. And the Republicans in the House, [said] you know what, we're in the minority. Even though it was their administration. And so there was some Republicans ideologically opposed to it, but there were many who just figured let the Democrats take the rap.

Dodd: This is, I think Barney and I agree on this thing. I don't think we ever did anything in my 30 years in the Senate as unpopular as this, and yet as more important as the TARP bill.

Brancaccio: You are sticking with that, even now?

Dodd: Absolutely. Had we not done that? What we didn't do well enough, and I blame the administration for a lot of this here, it always should have been a consumer bottom up approach to this thing. [It’s] about consumers and the country. And we too often, the language was always about stability of the institutions, and consumers kind of came in last.

Brancaccio: Well, you spoke up about that in some key meetings saying that's what this should be about. What was the reaction?

Dodd: To this day, it’s considered — despite the fact billions have been returned, consumers have been made whole in many cases — it's still seen as a bailout of financial institutions, and why didn't more people go to jail? We get that question almost daily.

Frank: The point is we did write that, and we wrote the bill, so we wrote in authority to limit compensation to the top people. We wrote in the requirements that they not just repay the loan with interest, but we have the warrants that Chris mentioned, in case there were profits. We wrote in a mandate to do something about foreclosure. And here was our dilemma — at that point the Republicans were running the show, and you can't run a program from Congress. You can authorize it. You can give them the tools, but you can't wield them yourselves. And the alternative for us would have been not to give them the authority. I mean the idea would have been to give them the authority, to have them use it. But giving the authority, even though they weren't going to fully use it in ways that we like, it was still a better choice than not giving the authority at all and having a crash. And that was our frustration. And its limitations of being in the legislative body. They had their hands on the tools.

Dodd: There's some remarkable stories though out of this. I’ll share with you, that night of the vote. I asked everyone to vote from their seats in the Senate which we rarely do. And I went around to members who were up in 40 days, Democrats and Republicans.

Brancaccio: Were up for re-election in 40 days ...

Dodd: I knew I had 75 votes. Sen. Kennedy was very sick and he was going to be the missing vote that evening, he wasn’t back. So the vote was 75 to 24. But I went to Democrats and Republicans, said, I'll never repeat your name or use your name, but if you want to vote no on this thing, I've got the votes. If I needed your vote, I’d tell you I did. And I’ll never forget, Gordon Smith, Republican from Oregon. I made him the same offer. He said, “great offer,” he said, “but I've got to see a constituent the morning and I don't know quite how I explain it, to be honest.” I said, “who is the constituent in the morning?” He said, I'll never forget this, he said, “the mirror.”

Brancaccio: The mirror, he has to look in the mirror.

Dodd: And as a result, he lost 40 days later. Bob Bennett ultimately lost in Utah, Kay Bailey Hutchison, you point out, in Texas. Mike Castle in Delaware. Four years later, this was still a major campaign ad against anyone who voted for it.

Frank: You mentioned, you know that maybe it was rational. Yeah it was rational in your own self-interest. Chris and I knew this was not the most popular thing. My staff did. You know, I look, when I had my toughest race when I first ran for office in 1980. But my second toughest race was my last race, in 2010, because we had passed a wonderful bill and we had done these things. But it was very unpopular, and the problem is, it's hard to get political credit for averting disaster. I mean, I complain about, my staff actually made up one copy of the bumper sticker I said I wanted to use. They were afraid I would use it. It said here's what I want to run on, “things would have sucked worse without me.” But you don't get any credit for that. But on the other hand, to make your point Chris just told you, that reaction was a major piece of the rightward movement of the Republican party because Republicans who voted for the legislation suffered badly in 2010.

Brancaccio: And more conservative people replaced them.

Frank: And that, and as Chris also pointed out, you know things don't go away. The 2010 Republican primaries, I think, terrorized an awful lot of Republicans, and it’s a major factor in the Republican Party having moved that way to the right.

Brancaccio: Well I'm going to pick up on that theme in a second, about the Republican Party and Trump and the financial crisis. We'll get to that. But let me ask you something. Part of this idea of it's so deeply unpopular, but, Sen. Dodd, you point out you think it was crucial that you did it at the time.

Dodd: Absolutely. No question.

Brancaccio: But what part of, do you want a second Great Depression or not, wasn't made clear to people?

Frank: We tried, but they didn't believe it.

Brancaccio: Or, maybe you couldn’t though because people were afraid of rattling the markets.

Frank: No, by then—

Dodd: Even worse than that, It’s one thing that they didn't believe it then. We're both blessed and burdened with no memory in this country. And that’s an asset and a liability. And when you go back and tell people five million homes went into foreclosure, $13 trillion of national wealth evaporated, 27 million people lost their jobs, iconic institutions, investment banks, commercial banks, credit unions, savings and loan, disappeared or nationalized or merged. It was an incredible set of issues that came to be. And people even today, you have to remind them of that to understand how much trouble we were actually in. And that, let alone today which is harder.

Frank: And it's hard to persuade people, as I said, that we’re going to have disaster. Americans thought well of the economy. By the way there's one other factor on the foreclosure — yes, we get the worst of both worlds on foreclosure. I think the reaction to that gave us two political phenomena: The Tea Party and Occupy. Because there were some people who were furious because we did some help for people, which we talked about. The Tea Party grew out of what's-the-guy's-name from CNBC. He said, “we need a Tea Party, how dare they help these people with their mortgages? Nobody helped me with mine.” So we had people on the right upset because we were talking about helping people avoid foreclosure. And then you had people on the left angry because we didn't help people do that.

Brancaccio: But the Tea Party turned this into an electoral movement. Occupy Wall Street was more ambivalent —

Dodd: Be careful about that line, you’ve got a great line.

Brancaccio: I would love to hear the line.

Frank: Here it is. Here was the problem, we had two movements came out of it: Tea Party on the right and Occupy on the left. And our problem was that the Tea Party registered to vote and got involved in primaries and took over the Republican Party. And the Occupy people smoked dope and had drum circles. And I will tell you that members of Congress are much more attuned to people who register and vote in primaries, than the people who sit around smoking weed and beating on drums.

Brancaccio: But they figured that out now, on the left side.

Frank: Finally, they didn’t then. I was on the Bill Maher show with a representative of Occupy, they didn’t have representatives, a person from Occupy, and I said, “well one of the things that troubled me was I never saw a voter registration table at an Occupy site.” She said, “well, we weren't into that.” I agree that I think the left has learned now the lessons of 2016 and elsewhere. So people are going to be turning out. That's one of the things that I hope is going to be transformative this year.

Brancaccio: Well let me turn up the heat on this particular idea. Without the Great Financial Crisis that you two helped fight, without the crisis, do we get President Donald Trump?

Dodd: Well look, in my view I agree with Barney and others who made the case — but, arguably, it began with the Vietnam war. I think frankly, the health care debate had more to do — that month of August in 2009, a year later. It obviously didn't spring entirely [from] there, but they really, the town hall meetings that took over. No one was talking about the financial reform bill in September of ‘09. It was really all health care.

Brancaccio: So by a year later, we’re talking health care.

Dodd: But we're also talking about a time when, despite the fact that there were Republicans in the House and Senate who were obnoxious about these bills, the fact is that people like Judd Gregg and I worked on the TARP legislation together, helped draft it. We were working with the Bush administration, with the Secretary of the Treasury, putting this together. That image, 75 people in the Senate actually vote for TARP despite how unpopular it is, that Congress was demonstrating what it was capable of doing with good leadership and resolving problems. So the image was not all negative. You really were demonstrating your capacity to deal with a major problem and come together in a bipartisan way to do it. That wasn’t a bad message for the country.

Frank: What Chris said is very powerful and should be underlined. Here's the problem, there was a sequence. The TARP, the bailout as it was called, was very prominent. Unfortunately, we never got as much attention for what followed in that sequence, which was the toughest financial reform and regulation since the New Deal because health care took it off — it’s like the public, the media can only focus on one big issue at a time. And if we had the perception that the crisis was followed then by reforms to clean up the thing, we might have been better off, but health care intervened. So you never got — and Chris noted this, when you asked people what they thought about the financial reform bill, it’s the most popular bill that’s passed in a number of years. But you got to ask them, they don't bring it up because it was not as prominent. And as to Trump, I do think — look he won by so little. I mean we got Donald Trump because of less than 100,000 votes in Wisconsin, Pennsylvania, Michigan. Given that, a whole lot of things could have taken it. So I think the answer is yes. But here’s the trap I don't want us to get into. It wasn't the crisis that was the cause. It was the failure of policy that led to the crisis. And this is a frustration for us. It was the right wing policy of not regulating, of refusing to do regulation, of Greenspan refusing to use the powers he got. So the conservative philosophy brings on the crisis and then we as Democrats being responsible, step up and try to resolve it, working with some Republicans. And then we get blamed for it.

Dodd: And, we never could have, on the financial reform bill, if we had ever tried to pass it a year before we did, or a year after, it never would have happened. The window opened in that one moment and you either have enough sense to go through the window and get as much as you can done, or it closes very quickly and it wouldn't have opened up again in my view.

Brancaccio: So the law that has your, each of your names on it, it is very focused on fixing and shoring up the banking system, and making sure the banking system isn't as vulnerable the next time. Were you fighting the last battle, fighting the last war? Because what could happen next, God knows what could happen next, it could be something else.

Frank: No, the war was still on. The war wasn’t over. We ended the war. Yeah, it’s like saying, well when you were in World War II, when you were fighting Hitler, were you fighting the last war? No, we were fighting Hitler. What we were doing in the bill was — remember this stuff was ongoing. So what we were fighting was that, and yes we did, I think, substantially diminish the likelihood of those things happening again. We never said, nobody could say, that will be the end of everything. But it wasn't, this wasn't only looking back in history, we weren't fighting the problems of the New Deal, we were fighting an ongoing set of practices, and if we didn't put an end to them, they would have kept going.

Dodd: And there's several points underlying, which you cannot legislate, the lack of confidence, consumer confidence, investor confidence had been shattered because of what had occurred. And so what we try to do with the bill is not eliminate future crises, they are going to happen, but create tools, new tools, the ones that Bernanke and Paulson claimed they didn't have. So the stress tests for banks, the transparency in the derivatives market, the creation of the FSOC, so they could actually sit down together, consider that radical idea, and look over the horizon, and say are there product lines or institutions that are opposing systemic risk?

Brancaccio: This is what I often envision as like the war room watching over the financial system.

Dodd: The law says they have to meet four times a year, they’ve been meeting 30 times a year, on their own, because they realize the value of it. And that's a very critical, really a huge asset for the future.

Frank: And the thing that came out of the Senate with Jack Reed ... we created the Office of Financial Research, which was a set of experts whose sole function was to look ahead and see what the problems might be. And by the way the Trump administration, that’s one of the things which they have underfunded, they couldn't abolish it statutorily, because they they just don't believe that we should be as ready. And I would just add one other thing to that last answer that Chris gave, and that was — and this was one area that Paulson and Bernanke did complain to me and you saw it in Lehman and AIG, the opposites. When Lehman failed, they didn't do anything. When AIG was going to fail, they did everything. And what they said was their lawyers had told them, if a major institution couldn't pay its debts, they either had to let it go bankrupt and pay nothing, or step in and pay everything. And the key thing that we did and what’s called orderly liquidation, was to give them the authority, move in, take over the institution and pay only some of the debts, enough to keep things from spiraling out of control. And then levy on other financial institutions to get that money back. So that was another important piece of this.

Dodd: And one more piece, which Barney brought up last night, and they're still angry about it. “Too big to fail” — not only politically could you not get away with what we were able to do in 2008, but legally you cannot do it. They wanted to leave open the window, so that a major financial institution could get financial aid to bail them out.

Brancaccio: That there could be a future bailout.

Dodd: We shut it down. Now they could change the law.

Frank: In fact we teased them, and some of the experts, even, you know, Bernanke and Paulson and Geithner, who we work with, if you asked them, they’ve been supportive, and unlike a lot of other Republicans, they believe that what we did with derivatives, what we did with bank capital, what we did in these regulatory things were fine, but they are upset that we did shut down too strongly the possibility of unlimited infusion of taxpayer funds into failed institutions.

Brancaccio: Well, they just wrote a piece in common in The New York Times —

Frank: In fact, at the dinner they had last night, and Chris and I were there. And when they got through talking, I said maybe a little mischievously, “oh, by the way, I have a question for you guys. How you doing lining up sponsors for that bill you're pushing that's going to give back the authority to do all the bailouts?” And I got laughter in return.

Brancaccio: But this is a very serious point here, which is you didn't outlaw future crises.

Dodd: You can't do that.

Brancaccio: So something might happen, and what if they have to go back to congress?

Frank: A, the first place in a democracy, yes, sometimes you do. And by the way, we showed last time that there was a crash, that was Chris's point. They went to Congress and Congress responded in two ways, and we dealt with the crisis, and then we put in a pretty good set of rules. But, you can quote my husband, he says, “well first you guys were the EMTs, and then you were the surgeons.” And the result was a pretty good one. But here's the deal, we have given them the authority to intervene, but they have to put the institutions out of business, which some of the institutions don’t like. Here's the issue, we have said that you don't want unpaid debts spiraling through so that A can’t pay B, and then B can’t pay D, E, and F, and they can’t pay the others. But, they have to put the institution out of business. And what they said was, “maybe we don’t want to go that far.” And the other thing I would say is this: “if that's the issue, then the country has to decide it.” Well, let me make this explicit. What they've said is, what we did in there, the ability to put a major institution out of business and then pay only some of the debts — that's not going to work, because if a really big financial institution is threatened, there will be great political pressure to save it. So therefore, they would need the money to save it rather than put it out of business. And having gone through what we went through, we know that’s wrong. In fact, if a big financial institution was failing, there would be political pressure to shoot everybody in it, not to save them.

Dodd: You know, it's interesting because this was the vulnerability, politically, we faced all the way through this. The “too big to fail.” In fact there was memos passed around Republican circles, how to defeat the bill, say it's “too big to fail” is still alive and well. We actually lowered the threshold for financial supervision to $50 billion, which we just fundamentally changed. That was driven by Republicans because they constantly said “too big to fail” is still alive.

Put aside whether politically you can do it or not, subsequently that was the case. The very first amendment that passed the Senate in our consideration of the bill was offered by Richard Shelby and myself, which basically called an end to “too big to fail.” We had to emphasize that point — that “too big to fail.” Had we not done that, I think this would have been a difficult bill to pass, and I needed 60 votes, not 51. I needed 60. And all I got was 60 — one less and the bill is dead on this thing. But for Susan Collins, Olympia Snowe and the new Senator, Scott Brown from Massachusetts, we were able to get the 60th vote and pass the legislation. But “too big to fail” was always —

Frank: And what we put in instead, and it was in both versions — and we then had to reconcile it as we go into conference — no bank is “too big to fail.” They fail. What we have said is if they can't pay their debts, then we put them out of business.

Dodd: In an orderly way.

Frank: And that's what it’s called. And by the way, it anticipates that it may be that they've go so indebted that the federal government had to put in some money. But there's a mandate —the treasury secretary then has to get that back from others. But the other point is this: is that all the rules we put in about capital restrictions on bad loans, on restricting derivatives, requiring that derivatives be funded — we made it much less likely that they would have that degree of debt. But even if that fails and they do have more debt that they can pay off, they get put out of business and the debt is paid in part, not entirely, only as much as you have to, and we get that back.

Brancaccio: But what do you make of this, gentlemen. Marketplace, our show, was talking to Neel Kashkari, who you worked with during the great battles —

Dodd: Conversion on the road to Damascus.

Brancaccio: Oh, is that what happened? So he's the head of the Minneapolis Fed now, and he told us the other day, he thought — and this is a quote from him — “the biggest banks are absolutely still ‘too big to fail.’ If big banks ran into trouble today, the taxpayers would be on the hook because the administration will be faced with the same choice we were faced with,” I guess back them. “Let them collapse and potentially bring down the U.S. economy or use taxpayer money to bail them out.” And I think he said that people end up using taxpayer money to bail them out.

Frank: Two things about that. I think I called his bluff and he hasn't responded. He said over a year ago the banks were too big and had to be reduced in size. Did you ask him what size they should be reduced to? Because he doesn't answer that. What size?

Brancaccio: There's no answer to the idea of what is the right size?

Dodd: It’s not the size of a bank. It's whether or not they pose systemic risk. How much capital —

Frank: And how indebted are they? Look, Lehman Brothers was 750 billion. So the answer if you are not going to deal with the debt, they’re all too big, but he says he’s always abandoned that. But he just said what I told you they’re saying: he says if the bank is in trouble, you have to use taxpayer money. As a matter of fact, our law says that they can't.

Dodd: They cannot.

Frank: They would be breaking the law. In fact, that's what you just alluded to, the article that you saw from Bernanke, Paulson and Geithner. They are correcting Kashkari by pointing out that what he's afraid what happened can't happen under the law.

Dodd: Unless you change the law. Unless Congress changes the law.

Frank: Right. Instead, what you have to do — exactly right. And that’s what we tease them, because nobody’s going to help, we barely got anybody who’s going to vote for that new law.

What Kashkari mistakes is, that the law says you can't use taxpayer money to keep them alive. You can use taxpayer money to pay part of the debts after you have liquidated them, but then you get that money back from other financial institutions under the law. What he's saying and others are is, if it came to that — this is what I said to you — that would be too much political pressure and the administration in power would be afraid to use the law, and instead they would say, “Oh no, we can't let Bank X or bank Y, go under. We have to keep it alive.” And that totally misreads the politics of America.

Dodd: And not only that, but it’s a good point made earlier, because we're conscious of that. The orderly unraveling so that you have not the chaotic ripple effect throughout the industry, in a sense. We’ve set up a process whereby that can occur in a fashion that we think works.

Brancaccio: The living wills and all that stuff.

Dodd: And they’re doing it, FDIC, who handles the thing and knows how to do this and so forth. So again, we think that would help. So one, you can’t do it, Barney just said, but also, if it comes to that, we’ve set up the architecture that allows for that orderly dismantling of an institution.

Frank: Yeah, does he think they’re going to ignore the law? Again, you saw Bernanke, Paulson, and Geithner say, “No, you can’t do what Kashkari said is going to happen.” The other thing I do want to go back to, I was very disappointed in him, because he was talking about these banks were too big and we have to reduce them. And I asked him, I asked several people: how big is too big? There's no answer to that, because as Chris said, it's not the size alone isn’t the issue. The question is what kind of shape are they in? How indebted are they? Can they pay off the debts? And I don't know what Kashkari’s answer is. By the way, did he tell you what his response, what the solution is?

Brancaccio: No.

Frank: He said they’re “too big to fail.”

Brancaccio: He didn’t give us a number.

Dodd: Are Canadian banks too big? They’re larger than the U.S. banks.

Frank: And fewer. That’s why I’ve lost respect for Kashkari’s intellectual approach to this, because he says they’re “too big to fail.” What would he do about it? Does he — again, does he think they’re going to break the law? I can’t make sense out of what he’s saying.

Brancaccio: Let me switch topics here. In the law, you called it the Bureau of Consumer Financial Protection. It came to be known as the —

Frank: Consumer Financial Protection Bureau. The “Bureau” got switched.

Brancaccio: Yeah, it got switched recently. It’s being reined in by the present managers of it. What do you think: is it doomed, this thing you set up in Dodd-Frank?

Frank: It’s an outrage ... No, here’s the deal. As much as the conservatives hate it — and let’s be clear what they hate about it — it’s been very successful. Chris had the statistics we told you, how much money they brought in for people. There was this philosophy that —

Brancaccio: Well, $12.4 billion in relief to over 31 million consumers is the claim.

Frank: It goes back to Ronald Reagan’s government is not the answer to the problem. Government is the problem. It's deeply rooted in conservative philosophy that the private sector brings all the good, and the government does only harm. And here is a case where the government is protecting citizens against the private sector and they hate that the way the devil hates holy water. It absolutely hurts their theology. So that’s why they get so excited about what’s really not the major piece of the bill. And so what they're doing is not enforcing it. But here's the point: It's still so popular that for all that they hate it, there's been no legislative effort to diminish its powers or change its structure, unlike health care, where they kept doing that. And so yes, as long as Donald Trump is president, it won't use its powers. But as soon as you get a more sensible president, all those powers will be fully there to be renewed.

Brancaccio: But no legislative changes, but they are changing the CFPB’s ability. I’m just going to call it the Bureau from now on, that’s what you call it in the bill a lot of times. The Bureau.

Frank: But can I say something.

Brancaccio: Yeah.

Frank: Call it whatever you want. Who cares.

Brancaccio: [laughs] Maybe you needed a better name to start with. But the Bureau —

Frank: Are you serious? People get hung up on — that’s not the issue.

Brancaccio: Of course it’s not the issue.

Frank: But the point is this. Yes, they are not using it now, but it will be fully in effect the next time a president comes in who believes in it.

Dodd: Well, ‘cause we did — this is, let me just tell you. Having had a lot of meetings before we even got close to passing the financial reform bill, meeting with the top 13 financial institutions, a block or so from where we’re sitting today. And asking them, in preparation, what are the things that you’re most concerned about? There were two, in an hour-long meeting. Executive compensation and the Consumer Protection Bureau. That was it. That’s it. Those two. And I can tell you who’s in the room — you’d know every name in the room. And that was their concerns.

Frank: And it’s because it’s ideological. They hate the notion — this vindicated our view that the government can protect the citizens against abuse by the private sector with no harm to the economy. By the way, that’s the other point I want to stress right here. Trump and a few of his allies keep talking about how our bill has crippled the financial sector and done all this damage. But at the same time, they argue this is the strongest economy we’ve ever had. Now how is it possible to cripple a critical aspect of the economy, and still the economy works better than it ever did?

Dodd: And the two great arguments were: it’ll destroy profitability and lending. Profitability last quarter was $60 billion — $12 billion above the quarter over the previous quarter.

Brancaccio: Banks have been very profitable.

Dodd: Yeah.

Dodd: And the borrowing is $100 million more than the balance sheets going up. So people are lending money, the banks are profitable. And yeah, certainly the tax bill may have had some impact, but the idea that this bill that we passed was going to kill both profitability and lending is ridiculous.

Brancaccio: It’s just interesting to me that the Bureau is being cut back to the benefit, you would argue, the benefit of parts of the financial services industry that doesn't like it. But does the public — there's no outcry in support of the Bureau. This just isn’t happening.

Frank: A couple of reasons: first of all, it’s not that visible. It’s hard to demonstrate. Again, it is hard to demonstrate things that they should’ve done and didn’t. On the other hand, their recognition that it’s popular, they won’t let it be an issue. You say it’s being cut back; the powers are not being used. But what do they hate? Well, they don’t like that it’s funded automatically without going through the appropriations process.

Dodd: That’s the biggest problem.

Frank: They haven’t tried to change that. They don't like the fact that it’s a single director running a commission. They haven't tried to change that. They haven't legislated anything because none of them want to vote to cut it back. So if you simply have an administrator who doesn't use the authority, that's hard to dramatize.

Dodd: But you ask a good question, because I think this is what was clearly part of our thinking, and that is the funding scheme. Because what normally happens is so beyond the realm of news everyday, and that is starving an agency.

Brancaccio: Congress can tweak the purse strings if they don’t like something.

Dodd: And that’s how you kill them, you don’t kill them by — it’s no longer a question of a coup d’etat. It’s just slowly destroy the institution you can’t fund.

Brancaccio: But Congress can’t in the case of the Bureau. They can’t do it.

Frank: They cannot.

Dodd: And I would’ve frankly with the bill, I would have liked to have self-funded the SEC if we could. Because it certainly collects enough money to pay for itself every year, from bad behavior. And so we did this through the Federal Reserve system specifically, to avoid what they did with the Federal Trade Commission and others over the years. Starve them to death. And the public doesn’t really get that.

Frank: And that hasn’t changed. So I agree, yes, under Trump. But you know, by the way, that’s true of the Environmental Protection [Agency]. It’s true of a lot of things. You get people in power who don't believe in using the tools. There's no way you can force them to use them.

Brancaccio: I mean, you saw the head guy from the Bureau who does student loans quit not too long ago, he said they are not enforcing.

Frank: But again, the next time a president gets in office who believes in this, those powers are there. They have not been diminished going forward; they're not being used. And as far as popularity, yeah they tried to repeal the health care bill. They've tried to vote on other stuff. They try to repeal some other regulations. They haven't put the consumer bureau to one test because the Republicans don't want to vote on it.

Brancaccio: I want to go slightly back in time before we leave the subject, the Bureau. It does go back in time, but I didn't get the story from you, Chris Dodd. In late 2008, I think it is, before we're at crafting Dodd-Frank and we're dealing with TARP, you identified the crucial issue for the government's response to be something like restoring consumer confidence. But what was the story: apparently the other tycoons in the room with you didn't get what you were saying? They looked at you, what, blankly?

Dodd: No, and I’ll tell you another quick anecdote to make my point here. I was talking to a manager some years ago of sovereign wealth funds. This guy parked a huge amount of the country's money in our country. And I said, “Why do you do that?” I'm just curious why you do that. He settled for two reasons. He said, “First of all, you're pretty good at making money.” He said, but I want to tell you something. The second reason is actually more important than the first. He said and I will never forget what he said, “I have never lost a wink of sleep worrying about the fairness, the stability of the system. I've made money. I've lost money, but I've never worried about the integrity of the financial services system in the United States.” And what happened is we lost that reputation through all of this. And so confidence, while I can't legislate it, everything we had to do was designed to to restore confidence, hopefully, and secondly, to make sure that the policeman on the street if you will, the regulators, would have enough information to make good decisions. I can't force them to do that. They could disregard all of that if they want to. But don't ever tell me again we didn't give you the tools to identify a problem and respond to it accordingly.

Brancaccio: You would think think that would be self-evident, but apparently people didn’t understand what you were saying at first.

Dodd: It’s short-term thinking. It's quarter-to-quarter stuff. It’s I'll get my five years in and get out in a lot of cases, you know.

Brancaccio: I've got to go back to this thing about: without the financial crisis do we or do we not get Donald Trump? Regular human beings lost faith in the system. They think that maybe the social contract before the crisis was something like, “Well, let the plutocrats do what they got to do. But they’re watching out for us. They won't let it fall apart.” It started to fall apart and now people are like, “No, they're not watching.”

Dodd: You've got Turkey. You got Hungary. You got Poland. You got Austria. You’ve got the Philippines. You know, we're seeing, we're seeing, you know, this kind of governance emerge globally. It isn't just here.

Brancaccio: Nationalist governments.

Frank: The financial crisis accelerated it and accentuated it. But that's not the underlying problem. The underlying problem is the nature of growth in developed societies since the ‘80s, and this is now acknowledged, growth from the Depression through World War II with the post-war period — growth was good for everybody. We grew, developed economies in a way that helped the high-end people. It helped working people. They could go make glass, make autos, etc. And then beginning in the ‘80s, and this is, I think, fairly well-acknowledged, growth began to be a two-edged sword. It produced more overall wealth in a country but it exacerbated the way in which it was distributed. So if you were high-end in America or in other developed societies, if you had a lot of skills, a lot of education, sophisticated in technology, you made money. If your only working asset was an ability to go work hard, without a lot of skills, you got hurt. And so I think that's that's the basis for Trump or for Brexit or for the Five-Star Movement in Italy. It is that economic growth in the developed West has evolved to the point where it has a very unequal effect in the economy. And you have Thomas Piketty talking about how capitalism has become both an increaser of wealth and an increaser of inequity. Now what happened was and I do agree when you talk about the plutocrats. I think what happened was in 2010 the perception that the bailout was only for the banks and not others, convinced a lot of people that this unequal result was not simply the workings of an impersonal economy, but the elite was trying to screw them. So that added to it, but the underlying problem has been the economic reality and that's been an ongoing issue not just in America, but in — I was just reading a very good article by two economists at MIT in 2007 talking about how we are having this increasing inequality in this society and that is undermining faith in democracy.

Dodd: And someone comes along and promises that I can make you great again and sort of obliquely refer to a time that Barney just described here, when those opportunities existed and failing to recognize that automation and technology and all of these other matters have intervened in a way, making it difficult for that 50-year-old guy who’s just lost his job, who’s sitting in a VFW hall, and watching his kids move back into the house, and someone comes along and says: “I can solve your problems.”

Brancaccio: So are you two Democrats are going to let the Trump team offer their approach to this? I mean, because you've identified it as a similar problem.

Frank: That’s a silly question, I'm sorry.

Brancaccio: No, what I’m saying is —

Frank: What do you mean we’re going to let them?

Brancaccio: We’ve talked about the problem, so what is the response from your —

Frank: But why would you phrase it, are we going to let them?

Brancaccio: I’m teasing you.

Frank: Not very effectively. Let me just say —

Brancaccio: Not amused by my question, I stipulate. You didn’t complete your thought. The thought was: So what do you do about it from your perspective?

Frank: I do believe that the Democrats have to be more — well, here’s the deal. I do have differences with both Bill Clinton and Barack Obama, who each tried to do a lot to offset the unequalizing effect. But not enough. And I think what happened was, people on the liberal side have still accepted a framework in which growth is the dominant goal, and then recognizing that growth will cause some problems. After you promote growth, you then deal with the question of the inequality it brings. And I think you have to make them equal. And the example in both cases is trade. I wish that both Clinton — what Clinton and Obama both did with trade was say, “Look, trade is good. It helps the whole economy; it hurts some people. So let's pass a trade bill and then we will work on helping the people who were hurt.” And the problem was that the conservatives, specifically the Republicans said, “OK, we'll help you pass a trade bill but then when you want to do something to promote unions or to promote increased people's health care, we're not with you.” So I think going forward, the liberal position has to be, “Yes, we are going to promote economic growth, but integral to that, are going to be ways that we deal with the unfairness and offset that unfairness at the same time.”

Brancaccio: Even when mainstream economists say wait, dealing with inequality — that's inefficiency in economic terms.

Frank: Yes, and I think that's the mistake that mainstream economists have been making. I think there's a kind of — it's time to go beyond growth as the number one issue, and in America today, the fact is that — and this has been the case for 20 years and it's getting worse. Growth has a very unequal effect. And by the way, they may not like this and this goes back to what we were talking about before, what some of the business really has to understand is they don't have the option to do that anymore. I mean, they got Donald Trump. They got Brexit. They're getting the Five-Star Movement. I think it’s like what it was 90 years ago when there was —

Brancaccio: 90 years ago.

Frank: Nine, zero years ago there was a loss of faith in democracy because capitalism wasn't producing enough wealth. And you got change, and you got this new idea that governments had to produce wealth. And so then beginning in the ‘30s and then into the post-war period, OK, democracy looks OK now because it’s producing the wealth. But I think what we're seeing today is in some ways like that. That producing wealth is no longer enough to sustain faith in democracy. You've got to produce the wealth in a way that promotes fairness as well.

Dodd: And the language about dealing with the inequality, of taking care of the unemployed worker — that guy I just described — seems sort of flat to me. I mean, “we’ll have job training programs” or something, and we’ve used the same language for three or four decades.

Brancaccio: Well, Charles Schumer used it with his new way forward that he offered last year, which one of the three planks was job training.

Dodd: Seems hollow. I can’t imagine anybody after two years with an infrastructure, huge set of problems in the country. You would think both Republicans and Democrats, given the absolute need for infrastructure improvements and so forth, real jobs could be created, would make some sense to do it. But too often the language doesn’t seem to have the vitality that growth does. Economic growth.

Frank: Training is good. Retraining — a 57-year-old coal miner is probably not going to become a computer programmer. I mean, I couldn’t become one. There are other things Democrats have been talking about more — unions. A major factor in the erosion of the incomes of average people, economists now will agree has been the anti-union activity. And it’s frustrating to watch — Trump talks about the working people and does such anti-union stuff. But raising the minimum wage — I think you’re beginning to see. There are a couple of things that would help. Raising the minimum wage and helping people with their medical care costs. Expanding Medicare in some ways: lowering the age or having a public option. Those are things that, and I agree that — I think that both Obama and Clinton were slow. Clinton was slow to see the need to make sure that pro-growth and pro-fairness went together. But I don’t think, well, by the Obama administration, while the president was for trade, overwhelmingly Democrats were voting the other way, saying no, we gotta do the other. I think the next time you see a Democratic majority in the house or the Senate are going forward, and then the presidential campaign, there will be a much more explicit set of programs increasing health care, minimum wage, protecting unions, that deal with this.

Brancaccio: Let's get back to Dodd-Frank. This is one of the crucial achievements of both of you; it has each of your names on the bill, on the law.

Dodd: Originally the motion was to call the bill Frank-Dodd, and Barney pointed out at 4:30 in the morning, they’ll think it’s one person. We can’t have that out.

Brancaccio: Frank-Dodd.

Dodd: Yeah.

Brancaccio: Good old Frank Dodd. Who is he? Was he in the House or Senate? You were fighting the war, you make the point in this discussion in real time as you’re working on that bill. So how much could you take on? But there’s a lot to worry about in the financial system that Dodd-Frank doesn’t fully address. A lot of financial stuff goes on outside of banks. In hedge funds, and money market funds. They call it the shadow banking system.

Frank: Well, the bill does give them the authority to deal with that. The bill doesn’t just regulate banks. And this is one of the things that we’re proud of. Chris talked about the Financial Stability Oversight Council. It gives them the right to go after activity, so they’ve done some stuff about money market funds. I was talking to Janet Yellen yesterday, who was concerned there may not be much willingness to use some of the authority they have. But the F-Dodd did make some changes in the requirements for money market funds. So the law does not just cover banks, obviously it covers financial institutions. It doesn’t cover hedge funds as fully. That I agree with. But it has the right to step in if they see it as an issue.

Dodd: It’s a major problem. This is one of the major complaints of the bill: the fact that GE, Metlife and a few others — when we looked at these sort of non-shadow banking, not your classic definition, and that people have complained that this was overreaching in a sense. Now you can make a case, depending on the circumstances of each one, and there’s some legitimacy to that. But the pace of legislation allows, except in the area of hedge funds, for us to actually be directly involved with institutions that don’t specifically qualify as a bank.

Frank: Yeah, for instance GE, because of what we did, divested itself of its financial entity. GE started out as an industrial company. Then they went into being a big financial company, and to avoid the supervision they were getting, they divested. And even ask the hedge funds, hedge funds per se aren't regulated, but the financial instruments in which they deal are. For instance, derivatives. Nobody now can get involved in these massive derivative transactions putting nominally hundreds of billions at stake, without there being a protection against somebody incurring debt that they can't pay off. They go through exchanges. You have to post margin, you have to have capital.

Brancaccio: People may not understand that before Dodd-Frank, this is all kind of mysterious.

Dodd: Totally opaque.

Frank: Well, AIG, here's the story. AIG came to the Fed in September, and said, we have $85 billion in debt we can’t pay off. A week later, Bernanke said to us, “Oh, and we're going to need” — he was listing how much they needed for TARP — “we need $85 billion for AIG.” We said, “Oh, you already told us about that.” He said, “Oh, I’m sorry, that’s an additional $85 billion.” It turns out AIG was $170 billion in debt beyond what they could pay off, because they had been allowed to make promises without putting up the capital. And so what we changed in the law was, it would be literally impossible to go $170 billion in debt now without having some capital paid off. Just like you can’t — people know about margin for stocks. Well, yeah, you had to put up margins when you were buying stocks. You had to put up a certain percentage. But you could make a commitment with derivatives with nothing at all behind it. That’s not possible anymore.

Brancaccio: Did you follow this apparent loophole that's developed in Dodd-Frank, that if it was argued by the financial services industry that they could move some of their riskier trading, derivatives trading, to offshore foreign versions of themselves, and therefore beyond the reach of Dodd-Frank — and I think it was the CFTC was going to close the loophole. But that was just before the last presidential election. It's not closed.

Frank: Well, the law is still there. In fact, it's a really good point. They tried when we were still there to pass the law when the Republicans took over Congress. Well, part of the problem was we did not anticipate losing control of Congress in 2010. Because if we had kept that, we would have funded these things better. They had a bill that was going to exempt the overseas affiliates of American institutions from derivative regulation by the Commodity Futures Trading Commission. And then in the midst of that, the London whale surfaced, which was a loss by JPMorgan Chase, supposedly the best-run bank, of billions and billions of dollars and they didn’t even know how much it was. So the law was not changed. So you're right — they didn't complete the regulatory authority, but the statutory authority for the Commodity Futures Trading Commission to fully supervise those overseas activities hasn't changed.

Brancaccio: You've thought about this a lot, Congressman Frank, but I want to get you to address this because you just opened up this important area of inquiry, which is you can write a law, but you gotta enforce it. And as in the case that you mentioned in the 1990s of the Fed getting authority to better scrutinize the subprime market, and maybe Alan Greenspan wasn't as diligent as he should be doing that, does Dodd-Frank go far enough to make the regulators crack down?

Frank: It goes as far as you can. You can’t make — anybody do something.

Brancaccio: So is it a frustration that you can’t make them?

Dodd: But that’s always been the history. You go back to the banking laws of the 1930s. They were like 25 pages long. The rest was totally delegated to regulators. Imagine having votes? 51-49 votes on —

Brancaccio: On every little thing.

Frank: I don't like metaphors in general, but there’s one that’s very relevant. You can’t push on a string. I mean, it’s always the case you can stop people from doing bad things. But I don’t know how you could do much more. Especially since some of them are necessarily qualitative. I will say this though, even with the Trump administration, that bill is being administered much better than people might have thought, and the system is being run much more soundly and safely than it was before the bill was passed. And the reason is that the powers are there, and unless you’re a pretty irresponsible guy or woman, and you’re in charge of an agency, and it has the powers to do something — you’re going to be a little worried in the back of your mind that if you vigorously don’t use those powers and something goes wrong, you’re going to be in trouble. I do think the Trump people probably are, some of them may be more willing to hold back. But the powers — and by the way, if you look at some of regulators, Jay Powell, the new head of the Federal Reserve —

Dodd: Very good.

Frank: There’s no difference between the way he is administering those powers and the way Janet Yellen is.

Dodd: Done a good job. Well, Jay Powell I think is very good. We’re lucky to have him in that job. But I was going to make a case exactly to your point. I mean, you may have recently heard that the Consumer Protection Bureau was issuing a regulation to ban these sort of mandates that you have on arbitration. Where you couldn’t sue somebody, you had to agree to arbitration. And of course, the law gives the agency the right to do that. What they’ve done of course is challenge that successfully. So today, when you sign these agreements here, you’re signing clauses here that require you individually to arbitrate. Not collectively do so or file a lawsuit. There’s an example where the law still gives the agency the opportunity to regulate, but regulations will be subject to jurisprudence and our ability to prohibit them from doing so would be unconstitutional.

Brancaccio: We're talking about inequality before, I haven't asked you more directly about executive compensation. Average pay for all CEOs is up 72 percent between '09 and last year. Last couple of years, some, if not a lot, of that jump has been the rising stock market. But the typical worker's pay is essentially flat, it keeps staying essentially flat. Dodd-Frank deals with that through, the main mechanism is transparency, right? That's what you tried to do?

Dodd: Well, “Say on Pay,” we don't force it. But I know they don't like it. Once every three years, the boards can vote on these things here. It's a, you know, it's a difficult area to legislate in because the opposition was so strong to this. I mentioned earlier to you the two issues that I was told over were again: compensation and the Consumer Protection Bureau were the two really big points to this.

Frank: We gave the shareholders the right to control the top executive compensation. On the whole, they haven't used it, again. But they have used it some. Vikram Pandit lost his job as a CEO of Citicorp because of a negative vote on pay, and there have been some cases where it has been, has been used. I noticed The Economist magazine, which didn't like the law because they really have have a great free enterprise. They hate to admit that the government was needed. But they, in their most recent analysis, say yeah, the "Say on Pay" has restricted — and "Say on Pay" goes beyond transparency. It lets the shareholders vote every year, and they can do it as much — if they want to wait till every three years — but they have to give the shareholders a vote at least once every three years on the compensation of the top executives and the shareholders can can vote no and nobody's going to defy that. The other is publishing the ratio, which is — Sen. Bob Menendez pushed for that.

Brancaccio: The CEO pay over the typical worker's pay — the average worker.

Frank: And while it's not binding, apparently it had some effect because the CEOs hated it like poison.

Brancaccio: Well the argument — you know what the argument is. The argument is: It makes CEOs look especially bad if it's a type of industry that has a lot of lower-paid workers.

Frank: Well, than if I were them, I'd go to work in another industry. I mean, the notion that, “Oh, poor CEO who's making $27 million, we hurt his feelings.” That's tough. If you have —

Brancaccio: It is very embarrassing though when you show up on the wrong part of that list.

Frank: Take another job. But by the way, live on $20 million instead of 27.

Dodd: A related issue that, again, this doesn't get a lot of attention, obviously, the "Say on Pay." Also related to that is the whistleblower provisions in the bill, which here again was controversial, and frankly, I think Barney and I both had our reservations a bit about it. The idea that we'd probably see a deluge of whistleblowing accusations because you can bypass the business you work for and go directly to the SEC.

Frank: With anonymity.

Dodd: With anonymity. And, of course, the SEC was worried about it. It turned out all of our fears, whatever fears we had, nonexistent. They've been a great success and made a difference in the last several years.

Frank: And by the way, again, when you go back —

Dodd: Are you familiar with the position?

Brancaccio: Yeah, absolutely.

Frank: You know, yes, we tried to cap CEO pay or at least restrain CEO pay, but more importantly, we were trying to raise the pay of the workers with unions and better taxation and with other factors that would increase their pay.

Brancaccio: Because, you know, early on you lived through that, when the AIG bonuses happened. That that did not make anybody's life easier except for the people who got their bonus in the end. But do you think in a sense the outrage that erupted when AIG still paid out the bonuses may have helped you with the broader reform?

Frank: No, I think it just made people angrier, and anger is not —

Brancaccio: Well, you harness some of the anger for reform.

Frank: Yeah, well the reform — actually, what helped us particularly in April of 2010, the Senate was taking up the bill — we'd done it in 2009 — you had the Goldman Sachs fiasco, where it turned out they had bet against some of the things they were selling people. They were selling citizens certain investments and then themselves making investments that assume the things they were selling wouldn't do well. And Sen. Carl Levin, who was a great investigator, had a very good hearing on that. So that thing, that helped us.

Brancaccio: So gentlemen, they're tinkering with your Dodd-Frank, and Congressman Frank, you don't seem to mind too much.

Frank: No, Chris and I were very much unbothered. If you go back to that, the change they made we both disagreed — we had a $50 billion limit on when you went into supervision —

Dodd: Because the Republicans drove us to that. (chuckles)

Frank: We both felt 100, 125 would have been OK. They went for 125. They went to 250. So there were maybe, I don't know, a dozen banks.

Brancaccio: Essentially, we're talking about the size of the bank at which they are subject to the most strict —

Dodd: Heightened supervision.

Frank: But they still — the other rules are still there. They're still subject to the Volcker rule about not using their own money for derivatives. They're still subject to the restrictions that say you have to have more capital. The major thing that bill did was to relax the rules for the banks of 10 billion and under, which are the ones that have real political clout. And if you go back and look at what people like Sen. Warren and others were afraid of, many of them would say it wasn't just what was being done in that bill. They were afraid this was the beginning of a process of nibbling away —

Brancaccio: The thin end of the wedge.

Frank: Yeah, and it turned out that wasn't the case. That was the, that was the total wedge, and that's what makes us feel more secure. That passage of that fairly small change was the last change that's going to happen. It changed the political dynamic. The Democratic senators who pushed for that now feel totally secure in not having to support any other change and that there will be no further change to the law.

Brancaccio: Because it was community banks, there's a lot of them and they have the clout.

Frank: They're in everybody's district.

Dodd: And for the bill, Dodd-Frank. Cam Fine, who runs the association, we dealt with him on a daily basis. The community banks supported the Dodd-Frank legislation. But let me also mention to you that Jay Powell points out the Federal Reserve has maintained its jurisdiction for heightened supervision of lending institutions being audited between 50 and 250. And Jay Powell is not going to give that up. And so even though they did this in the bill, per se, the Federal Reserve remains, maintains that ability.

Frank: Basically what they did in the bill, as Chris said, they kind of bought off the small banks. Ten billion is not tiny, but they're the ones in everybody's district, and they sponsor the Little League, and they have those crazy TV commercials. But the result is that there is now no significant political pressure to weaken anything else, and with regard to the biggest banks there was no change, there's no relaxation of the rules on derivatives, for example, no weakening of the consumer bureau legislation. So I think what we now have is a confirmation that 90 plus percent of that law is going to remain on the books.

Dodd: There are 5,000 banks in the country. There are 111 of them that have assets in excess of 10 billion. You know, the irony here is, only in Washington would you consider a small bank a bank that has $10 billion in it. I mean, you know.

Brancaccio: You're not partial to the change, Mr. Frank? Because you sit on the board of Signature Bank, that's a medium-sized bank. They might stand to profit from this.

Frank: Yes, and in 2013, before I had ever heard of Signature Bank, Dan Tarullo, who was the best regulator I thought at the Federal Reserve, in a speech in Chicago, said that he thought the 50 billion was too low and should be raised to 100 billion. And he said he thought the banks that had less than 10 billion in assets should be exempt from the Volcker rule. And again, before I'd ever heard of Signature Bank, I said publicly that I thought that was absolutely right. And so yes, I then went on to the board of a bank several years later that would have been affected by the 50 billion, but it had no effect on my position because I had said several years publicly before that, I had written that, that I was for that change.

Brancaccio: While we're talking about careers here in 2008, here in 2018, Chris Dodd, you joined a law firm that does consulting here?

Dodd: Well, they're a large law firm. They do a lot more. There are a lot of practices, but financial services is one of the practices. You're a reporter. Since you've raised it, you can't just say a firm. I want to give them proper attention here.

Brancaccio: Arnold & Porter.

Dodd: Arnold & Porter is a great law firm going back years.

Brancaccio: But do they use your position there to roll back Dodd-Frank?

Dodd: No, of course not. In fact they've been great. I've joined on amicus briefs and so forth which support our legislation, and obviously they don't have a huge client base that ... that isn't necessarily in favor of Dodd-Frank, but that's not unique to that law firm or any law firm.

Brancaccio: So, the implication of my question is, is there a conflict of interest, you sitting on the board at Signature Bank?

Frank: Yeah, and I want to say one I have been strongly for the tough regulation, but the best thing that happened to the bank of which I am a board member in the past few years was the Trump tax cut, which benefited that bank.

Brancaccio: And you're opposed ... You were opposed to that tax cut.

Frank: I did as much as I could to oppose that tax cut. And that was... If I was going to be guided by the bank's financial interest, I would ... I would have been a supporter of the tax cut. Instead I did whatever I could to urge people to vote against it.

Brancaccio: All right big picture here. We've been talking about the achievements of the Dodd-Frank law. But what worries you most now about the financial system? Surely, your worries are not over.